Understanding Strike Price Selection in Commodity Options Trades

By : Admin -

Understanding Strike Price Selection in Commodity Options Trades

When engaging in commodity options trading, one of the fundamental aspects to comprehend is the selection of the strike price. A strike price is the agreed-upon price at which the option holder may buy, in the case of a call option, or sell, in the case of a put option, the underlying futures contract or physical commodity. The strike price determines how the option will respond to movements in the underlying market and directly influences both risk exposure and return potential. A structured approach to strike price selection is therefore central to effective strategy design in commodity options markets.

Commodity options differ from equity options in several important ways, including the nature of the underlying asset, contract specifications, seasonal cycles, and sensitivity to macroeconomic forces. Agricultural commodities may be influenced by weather forecasts and harvest data, energy products may respond to geopolitical developments and inventory reports, and metals often react to currency movements and industrial demand indicators. These characteristics shape how traders evaluate strike levels. Selecting an appropriate strike price requires integrating price expectations, volatility analysis, time decay considerations, and capital allocation constraints.

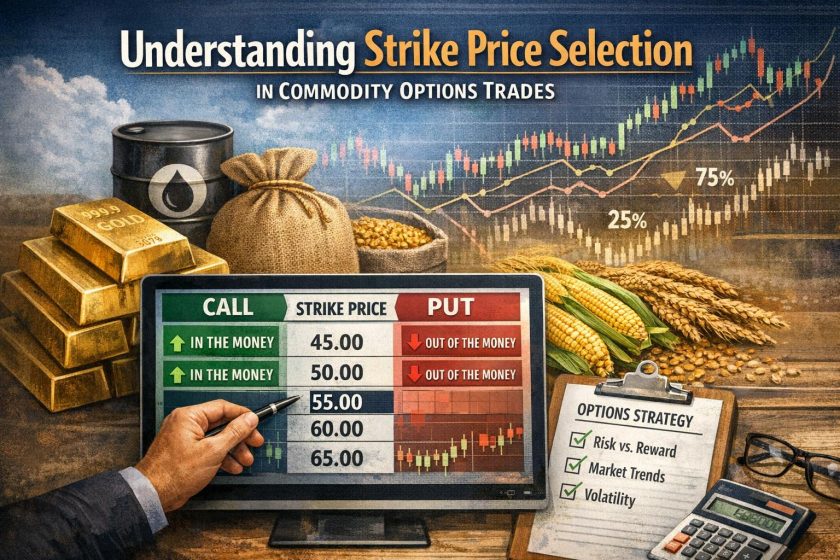

What Is a Strike Price?

The strike price, also referred to as the exercise price, defines the level at which the option can be exercised. For a call option, exercising allows the holder to purchase the underlying futures contract at the strike price. For a put option, exercising allows the holder to sell the underlying futures contract at the strike price. The strike is fixed when the option is initiated and remains constant throughout the contract’s life.

Each strike price produces a distinct risk and reward profile. If the market price of the underlying commodity moves beyond the strike level, the option may gain intrinsic value. If it does not, the option’s value may erode as expiration approaches. The relationship between the strike price and the current market price defines whether the option is categorized as in-the-money, at-the-money, or out-of-the-money. These classifications are not static descriptions but rather dynamic conditions that evolve as the underlying market fluctuates.

In practical terms, strike selection is a matter of probability assessment. Traders estimate the likelihood that the commodity’s price will reach or exceed a particular strike before expiration. This probability, combined with the cost of the option premium, helps determine whether the trade offers an acceptable expected return relative to risk.

Components of Option Value and Their Relation to Strike

To understand strike price selection, it is useful to examine how option value is constructed. The total premium of a commodity option consists of intrinsic value and extrinsic value. Intrinsic value exists when an option is in-the-money. For example, a crude oil call option with a strike of 70 trading when the futures price is 75 has intrinsic value of 5. If the futures price is below the strike, the call has no intrinsic value.

Extrinsic value, often referred to as time value, reflects market expectations about volatility, time remaining to expiration, interest rates, and supply-demand conditions. The further a strike is from the current price, the lower its intrinsic value and typically the lower its overall premium, though implied volatility plays a substantial role. Deep out-of-the-money options may consist entirely of extrinsic value.

Strike selection directly impacts the balance between intrinsic and extrinsic value. Options closer to the money generally have higher deltas, meaning their prices move more closely in line with the underlying. Farther out-of-the-money options have lower deltas and respond less to small price changes. Consequently, traders selecting strikes are also implicitly selecting sensitivity to market movements.

Factors Influencing Strike Price Selection

Market Volatility

Volatility is a primary determinant of option pricing and a central consideration in strike selection. In commodity markets, volatility may fluctuate due to seasonal patterns, policy announcements, weather developments, or shifts in global demand. Higher implied volatility increases premium levels across strike prices, but the relative pricing of different strikes may also change.

When implied volatility is elevated, out-of-the-money strikes can become relatively expensive because the probability distribution of future prices widens. Traders expecting volatility to decrease may prefer strikes that benefit from time decay and volatility compression. Conversely, if future volatility is expected to increase due to an upcoming report or geopolitical event, traders may choose strikes that offer leveraged exposure to large price swings.

Historical volatility analysis provides context, but implied volatility reflects current market consensus about future uncertainty. Comparing these measures helps determine whether certain strikes appear mispriced relative to expectations.

Time to Expiry

The time remaining until expiration shapes the probability that a given strike will become profitable. Longer-dated options allow more time for commodity prices to reach distant strike levels. This added time increases premium cost but enhances flexibility. Strike selection in long-dated options often reflects broader structural views about supply-demand imbalances, inflation trends, or monetary policy.

In shorter-dated options, time decay accelerates as expiration approaches. Traders selecting strikes near expiration must evaluate whether the expected price movement can occur within a limited timeframe. Out-of-the-money strikes may require substantial and rapid price movement to become profitable before time value dissipates.

The interaction between strike distance and time horizon is crucial. A strike that appears ambitious in a one-month contract may be more reasonable in a six-month contract if the underlying commodity has historically displayed wide cyclical swings.

Risk Appetite and Capital Allocation

Risk tolerance plays a defining role in strike selection. In-the-money options require higher upfront premiums but typically have higher probabilities of expiring with value. Out-of-the-money options demand lower premium outlays but may expire worthless if the anticipated move does not occur.

Capital allocation considerations also influence strike choice. Traders seeking defined risk exposure may allocate a fixed premium budget and select the strike that offers the most suitable balance between probability and payoff within that constraint. Institutional participants managing portfolios often adjust strike selection to maintain risk metrics within predetermined limits, such as value-at-risk or margin utilization thresholds.

In commodity hedging applications, strike selection may be influenced by operational requirements rather than pure speculation. A producer hedging future output may choose a strike aligned with cost of production, ensuring protection below a certain revenue threshold.

Market Structure and Seasonal Patterns

Commodity markets often exhibit seasonality. Agricultural markets may display predictable volatility during planting and harvest periods. Energy markets may respond to seasonal demand for heating or cooling. These cyclical characteristics affect the likelihood that certain price ranges will be breached within specific timeframes.

Strike selection in these markets frequently reflects awareness of historical price bands and seasonal tendencies. For example, an agricultural trader may choose a strike slightly beyond typical seasonal highs to reduce premium cost while still positioning for an above-average price year. Awareness of historical support and resistance levels also shapes decisions, as strikes near these levels may align with technical trading perspectives.

Strategic Approaches to Strike Selection

In-the-Money Options

Selecting an in-the-money (ITM) strike involves choosing a price that is already favorable relative to the current futures price. These options possess intrinsic value at initiation and usually exhibit higher deltas. As a result, they respond more directly to modest movements in the underlying commodity.

ITM options are commonly used when a trader seeks exposure similar to holding the futures contract but with limited downside risk equal to the premium paid. Because a larger portion of the premium consists of intrinsic value, time decay has a relatively smaller proportional impact compared to out-of-the-money options. However, the higher initial cost reduces leverage.

In commodity hedging contexts, ITM options may serve as insurance mechanisms. For example, a grain producer concerned about price declines might purchase puts with strikes slightly above the current price, securing a favorable minimum selling level.

At-the-Money Options

At-the-money (ATM) options have strike prices nearly equal to the prevailing futures price. These options typically contain the highest extrinsic value and are highly sensitive to changes in implied volatility. Their deltas are near 0.50 for calls or -0.50 for puts, indicating moderate responsiveness to price changes.

ATM strike selection is common in strategies designed to benefit from expected increases in volatility or significant directional movement. Because the strike is neither deeply in nor out of the money, it offers a balance between affordability and sensitivity. Traders who anticipate large price swings but are uncertain about direction may use ATM options in combination structures such as straddles, where strike alignment is central to payoff symmetry.

Out-of-the-Money Options

Out-of-the-money (OTM) options carry strike prices that are less favorable than the current market price. Calls have strikes above the market, and puts have strikes below. These options are less expensive and provide greater percentage return potential if the market moves sharply in the anticipated direction.

OTM strike selection is often associated with speculative positioning. Because the probability of expiring in-the-money is lower, these options may expire without value. However, in commodity markets known for episodic price spikes, such as natural gas or certain agricultural products, OTM options can provide cost-efficient exposure to rare but significant events.

The decision to select an OTM strike should reflect an evaluation of both expected magnitude and timing of price movements. Traders may analyze historical price ranges, implied probability distributions, and fundamental catalysts to judge the feasibility of reaching the chosen strike.

Quantitative Considerations in Strike Decisions

Professional traders frequently integrate quantitative metrics when selecting strike prices. The delta of an option approximates the probability that it will expire in-the-money and measures price sensitivity. Selecting a strike with a delta of 0.30, for example, implies roughly a 30 percent probability of finishing in-the-money under certain model assumptions.

Other metrics such as gamma, theta, and vega provide further insight into how the option’s value will respond to price changes, time decay, and shifts in implied volatility. Strike selection inherently determines these sensitivities. A trader anticipating stable prices but declining volatility may favor strikes with high theta and vega exposure, while a trader expecting sharp directional movement may focus on delta and gamma characteristics.

Option pricing models, including variants of the Black model used for futures options, allow estimation of theoretical values for different strikes. Comparing market premiums with theoretical estimates can identify potential mispricings.

Hedging Versus Speculative Objectives

Strike selection differs significantly between hedgers and speculators. A mining company seeking to stabilize revenue may select a put strike slightly below the current price to protect against adverse declines while limiting premium expenditure. The objective is risk mitigation, not maximization of option payoff.

By contrast, a speculative trader forecasting a supply disruption in the oil market may choose a call strike well above current prices to achieve high leverage at modest cost. The strike distance reflects both conviction and tolerance for loss of premium.

Spread strategies further illustrate how strike selection can tailor risk profiles. In a bull call spread, buying a lower strike call and selling a higher strike call caps both upside potential and premium cost. The spacing between strikes determines maximum gain and breakeven levels. Therefore, strike selection is not limited to single-option decisions but extends to coordinated positioning across multiple strikes.

Liquidity and Market Depth

Commodity option markets may vary in liquidity across different strike prices. Strikes close to the current futures price typically exhibit tighter bid-ask spreads and higher trading volume. More distant strikes may have wider spreads, which increases transaction cost.

Liquidity considerations influence strike selection, particularly for larger traders. Entering and exiting positions efficiently requires attention to market depth. Selecting a theoretically optimal strike may not be practical if liquidity constraints impede execution at reasonable prices.

Practical Evaluation Process

A structured evaluation of strike price selection generally involves assessing market direction, estimating magnitude of potential movement, analyzing implied volatility relative to historical norms, examining time horizon, and aligning trade parameters with capital constraints. This process integrates both qualitative and quantitative information.

Technical analysis tools, such as support and resistance levels or trend indicators, may inform directional expectations. Fundamental data, including inventory reports, supply forecasts, currency movements, and macroeconomic indicators, contribute to estimating potential price ranges. Each of these elements interacts with the selected strike.

Ongoing monitoring is also necessary. After initiating a trade, changes in volatility, time decay progression, and underlying price trends may justify adjustment or early exit. Strike selection is therefore part of a broader dynamic risk management process rather than a single static decision.

Final Considerations

Selecting the right strike price in commodity options trading requires a disciplined evaluation of price expectations, volatility conditions, time horizon, and financial objectives. The strike defines the payoff structure and shapes how the option responds to changes in the underlying commodity. Different strikes offer distinct combinations of probability, leverage, and premium cost.

Effective decision-making integrates knowledge of market fundamentals, statistical measures, liquidity conditions, and portfolio constraints. Whether the objective is hedging operational risk or pursuing speculative opportunity, strike price selection remains central to strategy design. By systematically analyzing these elements and aligning strike choice with defined objectives, traders can structure commodity options positions with clearer expectations of risk and potential return.

This article was last updated on: March 9, 2026