Using Vertical Spreads in Commodity Options to Define Risk and Reward

By : Admin -

Understanding Vertical Spreads in Commodity Options

Vertical spreads are a structured options strategy widely used in commodity markets to manage exposure to price fluctuations in assets such as crude oil, gold, natural gas, agricultural products, and industrial metals. Commodity markets are often characterized by volatility driven by supply and demand dynamics, geopolitical developments, seasonal cycles, and macroeconomic conditions. Within this environment, vertical spreads provide traders with a controlled framework for expressing directional views while defining both potential losses and potential gains in advance.

Unlike outright option purchases, which can expose traders to significant time decay and volatility shifts, vertical spreads combine two option positions into a single integrated strategy. The defining feature of a vertical spread is that both options share the same expiration date and underlying commodity but differ in strike price. This structural characteristic enables traders to modify the risk-reward profile of their position and tailor it to specific market expectations.

Structural Foundations of Vertical Spreads

A vertical spread consists of two options of the same type—either both calls or both puts—on the same commodity contract. One option is purchased, and the other is sold. The difference in strike prices determines the maximum potential profit and loss of the position. Because the expiration date is identical for both legs of the trade, the passage of time affects them simultaneously, which simplifies analysis relative to other multi-leg strategies.

In commodity options markets, underlying contracts are typically futures contracts. Therefore, a vertical spread in commodity options references a specific futures contract month. For example, a trader constructing a vertical spread in crude oil may use options on the December crude oil futures contract. The value of each option, and thus the spread, will respond to movements in that underlying futures price.

The fundamental objective of a vertical spread is to balance cost and opportunity. Purchasing a single call or put provides unlimited or substantial upside potential but requires paying a premium. By selling a second option at a different strike, the trader collects premium income, which offsets part of the initial cost. In exchange, the trader limits the maximum profit to the difference between the strike prices minus the net premium paid.

The term vertical refers to how the strategy is displayed on an option chain, where different strike prices are often listed vertically. Because both options share the same expiration date, the difference between them lies strictly in strike level rather than time.

Types of Vertical Spreads

The two principal categories of vertical spreads in commodity options are the bull call spread and the bear put spread. Both are debit spreads, meaning the trader pays a net premium to initiate the position.

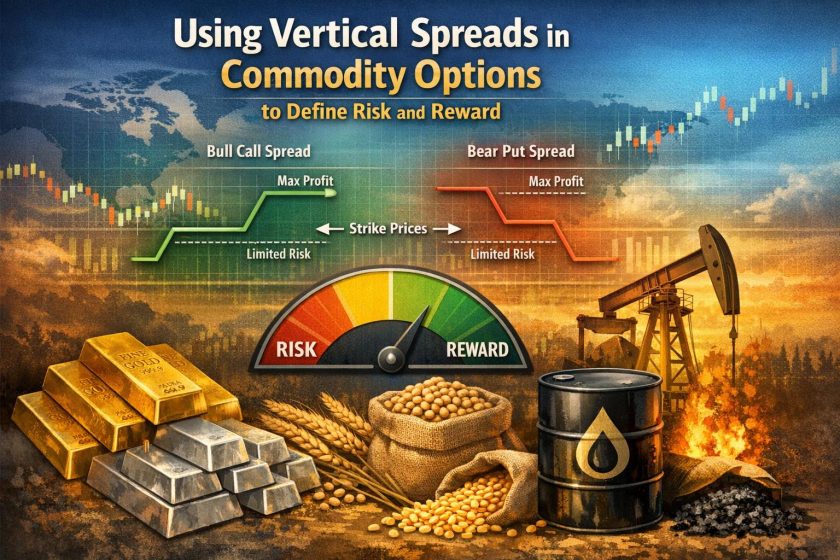

Bull Call Spread

A bull call spread is established when a trader buys a call option at a lower strike price and simultaneously sells a call option at a higher strike price, both with the same expiration. This strategy is appropriate when the trader expects a moderate rise in the price of the underlying commodity.

For instance, assume gold futures are trading at 2,000. A trader expecting a rise to around 2,080 could purchase a 2,000 call option and sell a 2,100 call option. The premium received from selling the higher strike call reduces the overall cost of the position. The maximum loss is limited to the net debit paid. The maximum gain is capped at the difference between the strike prices minus that net debit.

If gold futures rise significantly above 2,100 by expiration, gains do not increase beyond the defined maximum. This reflects the trade-off inherent in the strategy: reduced cost and risk in exchange for limited upside potential.

Bear Put Spread

A bear put spread is constructed by buying a put option at a higher strike price and selling a put option at a lower strike price, again with the same expiration. This spread is used when a trader anticipates a moderate decline in the commodity’s price.

Consider crude oil futures trading at 75. If a trader expects a move down to around 68, they might buy a 75 put and sell a 65 put. The short put generates premium income that offsets part of the expense of the long put. The maximum risk remains limited to the net premium paid, while the maximum profit equals the difference in strike prices minus that premium.

This approach is particularly relevant in commodity markets, where downward price movements can occur rapidly in response to supply expansions or weakening demand indicators. The bear put spread allows traders to participate in such moves while controlling cost.

Additional Vertical Spread Variations

Although bull call and bear put spreads are the most commonly referenced vertical spreads, traders may also use credit spreads in commodity options markets. These include bear call spreads and bull put spreads. In these cases, the trader receives a net premium at entry and assumes limited risk defined by the strike difference minus the credit received.

A bear call spread involves selling a lower strike call and buying a higher strike call. It is typically employed when the trader expects limited upside or a stable to declining market. Conversely, a bull put spread involves selling a higher strike put and buying a lower strike put, often used when the trader anticipates stable or moderately rising prices.

Whether structured as debit or credit spreads, vertical spreads in commodity markets provide consistent risk boundaries and established payoff profiles.

Risk and Reward Dynamics

One of the defining attributes of vertical spreads is that both maximum profit and maximum loss are calculable at initiation. The maximum loss for a debit spread equals the net premium paid. The maximum profit equals the strike price difference minus that premium. In credit spreads, the maximum profit equals the net credit received, and the maximum loss equals the strike difference minus the credit.

In commodity options trading, such predefined parameters are particularly valuable due to price volatility. Agricultural commodities may experience sudden swings due to weather conditions. Energy products can react sharply to geopolitical events. Metals may fluctuate in response to currency movements and industrial demand changes. Vertical spreads allow traders to participate in these markets without exposing themselves to unlimited risk.

The risk-reward relationship must be evaluated relative to the trader’s price expectation. If a trader anticipates only a modest move, purchasing a single option may be inefficient due to high premium costs and time decay. A vertical spread can align more closely with a specific price target by narrowing the profit zone to the expected range of movement.

Impact of Volatility and Time Decay

Commodity options prices are influenced not only by underlying price changes but also by implied volatility and time decay. Implied volatility reflects the market’s expectation of future price fluctuations. When implied volatility increases, option premiums generally rise.

In a vertical spread, the opposing option position partially offsets changes in implied volatility. For example, in a bull call spread, the trader is long one call and short another. If implied volatility rises, both calls tend to increase in value. The net effect on the spread is therefore smaller than the impact on a single long call. This moderating influence can reduce sensitivity to volatility shifts.

Time decay, measured by the option Greek theta, affects both legs of the position simultaneously. For debit spreads, time decay is typically negative but less pronounced than for outright long options. In credit spreads, time decay can work in the trader’s favor if the spread is structured to benefit from option premiums declining as expiration approaches.

Understanding how volatility and time decay influence vertical spreads is essential for traders operating in commodities where seasonal or cyclical volatility patterns may exist.

Margin and Capital Efficiency

Commodity futures and options trading often involves margin requirements. Exchanges and clearing firms determine margin levels based on anticipated risk. Because vertical spreads define maximum loss, margin requirements are typically lower than for naked option positions.

In a bull call or bear put spread, the maximum loss is limited to the net debit, which is paid upfront. In credit spreads, margin is generally equal to the maximum potential loss. This defined exposure enhances capital efficiency, as traders can allocate capital across multiple positions without assuming disproportionate risk in any single commodity.

For participants in markets such as agricultural futures, where contracts may represent substantial underlying value, maintaining precise control over margin usage is important for long-term sustainability.

Strategic Applications in Different Commodity Markets

Vertical spreads can be adapted to various commodity sectors depending on market structure and trading objectives. In energy markets, spreads may be used ahead of inventory reports or policy announcements. In agricultural markets, traders may target seasonal planting or harvest periods, when price moves tend to follow historical patterns.

In precious metals markets, spreads may align with macroeconomic outlooks such as changes in interest rates or currency valuations. Industrial metals traders may use vertical spreads when anticipating demand shifts linked to manufacturing activity.

By adjusting strike selection and expiration timing, vertical spreads can reflect short-term tactical views or medium-term outlooks tied to identifiable economic factors.

Transaction Costs and Market Liquidity

Although vertical spreads can enhance risk control, transaction costs must be considered. Because the strategy involves two option legs, brokerage commissions and exchange fees may be higher than for a single option trade. Liquidity in certain commodity options may also vary depending on strike selection and contract month.

Slippage between bid and ask prices can influence the effective cost of entering and exiting spreads. Traders operating in less liquid commodity contracts should carefully evaluate spread pricing and ensure that the anticipated risk-reward profile remains favorable after accounting for transactional friction.

Comparing Vertical Spreads with Alternative Strategies

Relative to outright futures positions, vertical spreads provide limited exposure to directional risk. Futures contracts offer linear returns, meaning profits and losses increase directly with price movement. In contrast, vertical spreads produce non-linear payoff structures with fixed ceilings and floors.

Compared to straddles or strangles, which aim to capture volatility irrespective of direction, vertical spreads are directional strategies. Their success depends on the commodity moving in the anticipated direction within a defined range. They do not benefit from large moves beyond the upper strike in a bull call spread or below the lower strike in a bear put spread.

Such comparison illustrates that vertical spreads are best suited for environments where moderate directional movement is expected rather than extreme volatility.

Expiration Outcomes and Settlement

At expiration, vertical spreads settle based on the intrinsic value of the component options. If both options expire out-of-the-money, a debit spread results in a total loss equal to the premium paid. If both expire in-the-money, the spread reaches its maximum valuation equal to the strike price difference.

Because commodity options may be physically settled into futures contracts or cash settled depending on exchange rules, traders must understand contract specifications. In many cases, closing the spread before expiration can eliminate potential assignment or delivery issues. Active monitoring near expiration is particularly important for credit spreads where short options may be exercised.

Risk Management and Position Sizing

Even though vertical spreads define maximum loss, prudent position sizing remains necessary. Commodity markets can experience unexpected gaps due to overnight developments, affecting liquidity and pricing. While the spread caps total risk, overexposure across multiple markets can still generate significant portfolio volatility.

Professional traders often calculate aggregate exposure relative to trading capital and ensure that combined maximum losses from multiple spreads remain within predetermined risk thresholds. This systematic approach supports consistent capital preservation.

Conclusion

Vertical spreads represent a structured and disciplined approach to trading commodity options. By combining long and short options of the same type and expiration but different strike prices, traders establish clearly defined boundaries for risk and profit. Whether implemented as a bull call spread in anticipation of rising prices or as a bear put spread in expectation of declining values, the strategy offers measurable outcomes and controlled capital commitment.

In commodity markets characterized by supply disruptions, seasonal dynamics, and global economic influences, managing exposure is central to sustainable participation. Vertical spreads provide a mechanism through which directional views can be expressed without assuming unlimited risk. Through careful selection of strike prices, attention to volatility conditions, and structured risk management, traders can integrate vertical spreads into broader commodity trading frameworks with clarity and precision.

This article was last updated on: July 16, 2026